Food for thought

The Pew Research Center’s FactTank recently published a greatest hits list of some of their most recent demographic findings. A few jumped out:

- Millennials are the nation’s largest living generation with 79.8 million compared with 74.1 baby boomers.

- Marriage among Americans has declined from 70 percent in 1950 to around 50 percent today. On the other hand, cohabiting relationships have increased 29 percent since 2007. A record number of Americans are living in multigenerational households.

- The US admitted nearly 85,000 refugees in fiscal year 2016, the most since 1999. More than half went to one of 10 states, with California and Texas receiving the largest share.

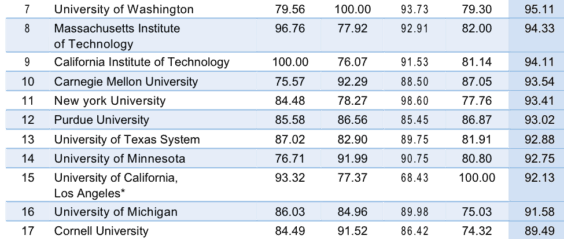

In the weeds

The regional Federal Reserve Banks have released an annual survey to examine small business financial needs. It is not a quick read, but several points stand out:

- 61 percent of the small firms surveyed faced financial challenges in the last year. The most common way firms cope with challenges is by self-funding—76 percent of business owners used personal funds to fill the gap. Firms also reported taking on additional debt (44 percent), making a late payment (44 percent), or downsizing (43 percent).

- 42 percent of small businesses rely exclusively on their owners’ personal credit scores to secure debt; another 45 percent use both the owners’ personal scores and business credit scores.

- Demand for financing was steady, with 45 percent of firms applying for funding, similar to 46 percent in 2015. Most firms (55 percent) were seeking $100,000 or less in financing; three quarters sought $250,000 or less.

- Eighty-six percent of credit applicants sought a loan or line of credit for their business; 31 percent applied for a credit card.

- Firms most frequently sought financing at large banks (50 percent), small banks (46 percent), and online lenders (21 percent).

- Five percent of applicants were approved for all of the financing sought, with financing shortfalls more common among smaller firms (annual revenues of $1M or less).

- Smaller firms apply most frequently to traditional lenders: large banks (49 percent) and small banks (42 percent). However, smaller firms are also notably less successful at obtaining financing from large banks (45 percent success) than they are at obtaining financing from smaller banks (60 percent success) or from online lenders (59 percent success). Successful applicants report greater satisfaction with credit unions (75 percent net satisfaction) and small banks (75 percent net satisfaction) than with large banks (46 percent net satisfaction) or online lenders (27 percent net satisfaction).

For your consideration

Several new online tools popped onto our radar this week. They require a little bit of user interface but could serve as a useful distraction during a committee hearing, an NBA playoff game or while sitting through a youth ballet rehearsal.

- Brookings has introduced a Metro Monitor Dashboard, which allows you explore different metrics related to economic opportunity. There is also a corresponding report, but the dashboard lets readers change inputs and variables and compare community performance.

- The Urban Institute has a county-based tool that allows for readers to examine data on rental housing, which it argues is in short supply. We wrote about the need for rental housing a little bit in our coverage of post-Matthew recovery efforts. This tool allows you to quickly compare county data. It, too, has a corresponding report for anyone interested in digging deeper.

- The Pew Research Center’s subdivision on Journalism & Media published a fascinating look at how their research team used Google search data to produce in-depth coverage of the water crisis in Flint, Michigan. It is a little more of a behind-the-scenes look than a data tool, but it give the enterprising wonk a peek at how search tools can feed research and news.

- We would be remiss not to self-promote a little here and remind you about our own state budgeting initiative, which uses the Balancing Act tool to let readers experiment with budgeting dynamics.

What we're reading